For CEOs and founders in the manufacturing industries, this presents a formidable opportunity for innovation as industries turn to software and automation to maintain and increase efficiency. One thing is clear: manufacturing in the second half of the 21st century won’t look like the first.

Having spent much of the past year at Inventure diving into this sector, I see a significant opportunity for both value creation and capture in the $16.7 trillion European and US manufacturing industries. There are unique challenges for founders in this space, but let’s dig into how they can be overcome, along with the areas we’re actively looking to invest in.

Before we go further, a huge thanks to former Sandvik, Luvata Vice President, and SECO Tools CEO Fredrik Vejgården; Cognite Vice President Andreas Steinsvoll Prøsch; iPercept founder Karoly Szipka; and former Sandvik and Aker Solutions Senior Vice President/Managing Director Hugo Nordell for sharing your thoughts and opinions.

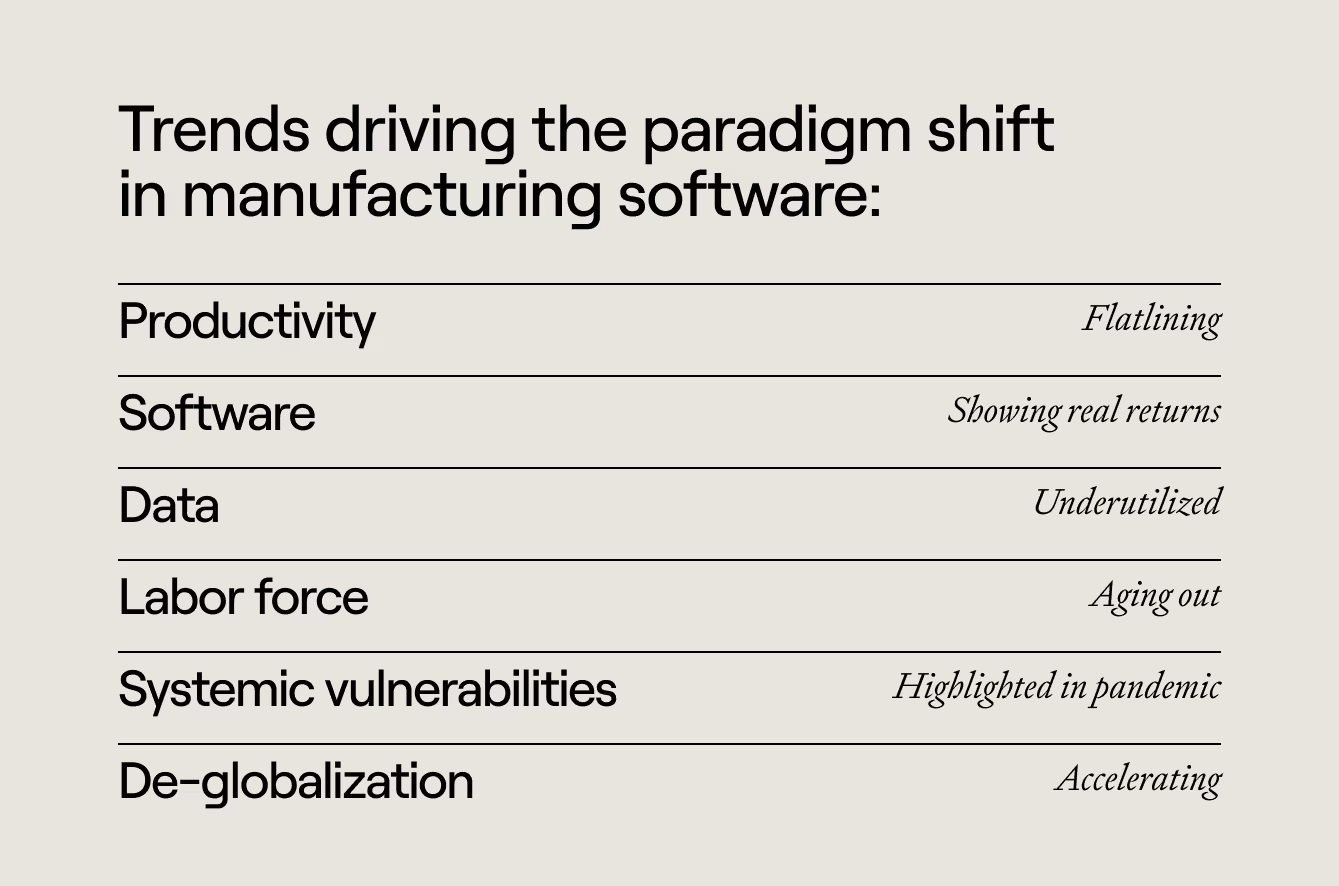

Here’s what’s propelling us into the next paradigm.

Productivity has flatlined

In the US, the productivity of industrial workers increased almost 50% over the last 20 years. But the driving force of these productivity improvements, such as Lean, Six Sigma and better hardware, have started to hit the ceiling. As an example of “marginal utility stagnation” in metal machining, new drills and equipment have started to hit physical limits for how efficient and effective they can become.

Software is the next move

With stagnating productivity, manufacturing industries are increasingly looking towards software and automation to unlock further competitive gains. This shift has already started, and research is showing major efficiency improvements for companies at the forefront. For example, a Bain study (Global Machinery & Equipment Report 2022) shows companies best-in-class in combining hardware and software solutions outperform the worst-in-class with 8x in total shareholder returns. Meanwhile, McKinsey (source) finds that in successful implementations of software and digital initiatives, it is not uncommon to see 30–50% reductions in machine downtime, 10–30% increases in throughput, 15–30% improvements in labor productivity.

There’s a massive amount of data to be leveraged

Due to the intrinsically process-driven nature of the industry, the manufacturing industry has twice the data of any other industry (Robin Dechant, GP Bullhound, Morgan Stanley). Europe has seen the first wave of companies such as Celonis and Cognite utilize this data with tremendous success. However — we’re very much in the early innings here. Immature software adoption and on-premise, siloed data is the rule, not the exception.

The manufacturing labor force is in terminal decline

Manufacturing companies today are already listing labor scarcity as a top 3 driver of downtime, and today’s kids aren’t dreaming of becoming manufacturing workers or machine operators. A quote from a precision metal manufacturing company says it all: “our youngest machine programmer is 55 years old”. As the labor force retires within the next decade, software will have to increasingly automate what is today done manually.

Covid-19 drove attention to vulnerability

The pandemic highlighted the vulnerabilities of internal and external supply chains and how person-dependent organizations are due to manual processes. We’re seeing a major mindset shift in factories’ sense of urgency to digitize because of this.

On top of all this — de-globalization is accelerating

For a long time, China has been the world’s manufacturing base due to the low labor costs and related margin advantages. As tensions rise in the Taiwanese strait, with the sanctions on Russian companies as a warning example, manufacturing companies need software and automation to maintain margins as they move their supply chains back home, or to friendly countries. The on-shoring or near-shoring has already started to materialize, and Bloomberg (source, source) reports that the construction of new manufacturing facilities in the US has soared 116% over the past year, dwarfing the 10% average increase across commercial building projects.

Large potential for category leadership

Building on the trends above, we’re looking at a unique moment for founders in the space. There’s a few factors intrinsic to the manufacturing industry providing fertile ground for industry-dominant category leaders:

Land-and-expand dynamics

If a startup can prove a new solution on one production line or in one factory, the customer is likely to roll it out across production lines, across factories and across geographies driving large customer values. Favorable upselling dynamics is a key factor we’re looking for.

Standardization = category leadership

Standardization defines the manufacturing industry. As one example, in metal machining, you’ll find 15% of machine brands in 80% of factories. Manufacturers are quick to implement proven and best-in-class solutions, paving the road to category leadership and market domination for the best companies able to break through.

Once you’re in, you’re in

Due to the high risk of implementing new solutions in a complex environment, once a solution is implemented, there are large switching costs and hence fantastic customer retention (the other side of the coin is longer sales cycles).

Value-based pricing

Compared to many other industries, manufacturing industries are used to value-based pricing to a higher degree, enabling software companies to capture a lot of the value they create (as long as they can credibly prove the value to the customer).

The go-to-market motion in the manufacturing space is different

How exactly you’ll get your new product into the industry’s hands is where doubts surface in the minds of founders and venture investors alike. Let’s dig into these challenges and how we think the best founders will overcome them:

Sales cycle challenges

Sales cycles in the manufacturing space are long and generally complex due to the high perceived risk of implementation. Downtime is incredibly costly (a minute of downtime costs an automotive manufacturer c. €22k, source), machinery is incredibly expensive, and there are many stakeholders involved in purchasing decisions. Moreover, many customers will be running on no or outdated software and may lack awareness of the potential of software and automation. This means that customer education will likely be needed parallel to battling the customers internal digital transformational inertia.

This has several implications for founders and investors in the space. The best teams will be able to sell as high as possible towards individuals with internal clout and credibility (e.g. Head of Manufacturing), providing a quicker decision-making path. Meanwhile, selling to innovation departments should be avoided, as they may in some cases be less involved in the operations and direct application of the software as well as purchasing decisions. During conversations, screen hard for signals of adoption readiness (e.g. ongoing digital initiatives) alongside problem awareness both at a factory manager level as well as within the executive management layer.

The perilous pilot purgatory

Pilots are a central part to both inform product development, as well as the obvious route to a recurring customer contract. However, all pilots are not created equal. According to McKinsey, only 30% of innovation initiatives make it to factory roll out, and the lion’s share of startups perish in what McKinsey (source) calls the “pilot purgatory” — running never-ending pilots and bending over backwards for the customer while never ultimately converting and rolling out the solution.

Finding the right customers to run pilots with are critical. While it can be easy to get a non-paid pilot due to customer’s desire to learn about new solutions, the complexity of taking software to market in this market premieres depth of a relationship with the right customer over quantity. This means optimizing for getting pilots where real user adoption can be generated, rather than pretty logos. There are multiple dimensions to the “right” customer.

Fredrik Vejgården, a former SVP at Sandvik, and former CEO of Swedish tool giant SECO Tools and now investor and advisor to startups in the space, elaborates:

“Segmentation is down to an individual level — finding the right type of person with the right mindset, working on the right processes aligned with your use case, to champion you internally.”

Moreover, founders need to be relentlessly driven by customer empathy. Manufacturers are incredibly value-driven, and if the business case isn’t crystal clear (and communicated in a way that makes sense for the stakeholders), the solution will never grab the attention of all stakeholders. Vejgården continues:

“As a startup in this space, you’ll end up right on the list of all other IT solutions and equipment investments, and the ROI is a core decision driver.”

Founders who solve one single problem, with a solution that easily can be tried across one product line (instead of a whole shop floor), and where the value easily can be calculated, will have an easier time going through the pilot motions. Pitching a platform — even though that might be the end-game you tell investors about — is going to trigger post-traumatic stress disorder in many factory managers. The’ll recall the painful implementation of SAP they started a decade ago, which took a decade to fully integrate, and ran way over budget!

Factory stack fragmentation

Founders and investors should expect that even factories within the same organization are different. Not only may factories be organizationally structured in different ways and with different decision-making dynamics, but different factories in the same company might have varying equipment setups (with different interfaces), alongside varying factory software stacks (e.g. different manufacturing execution systems, control systems and ERPs). At the same time, on-prem is still dominating in factories, meaning that data lives in silos and a unifying layer might be missing.

This means, if a solution requires too much tailoring and is sensitive to fragmentation in the software stacks across factories, this will hurt the land and expand dynamics and make roll-outs take more time. For founders, investing upfront in the ability to integrate with a wide range of different software stacks will be key.

“We got around the factory fragmentation issue through first of all spending a lot of time with a customer’s Head of IT to deeply understand the different interfaces and characteristics of the technology stack, and then investing a lot of time up-front in product development to work around it” — Karoly Szipka, iPercept Founder and CEO.

Bringing us into the next paradigm…

So what are we looking for? I’m excited about all sectors within manufacturing and industrial applications, but there are a few areas we’re looking into proactively.

Data infrastructure and insights

We’re very excited about solutions enabling more advanced analytics and interoperability across silos. There are incredible amounts of value to unlock through e.g. predictive maintenance and performance optimization, analytics providing overview across the full production process, real-time monitoring of workforce and equipment efficiency.

Workflow tools

As labor is scarce and getting scarcer, we’re excited about solutions that augment our manufacturing labor force with e.g. low and no-code tools for process optimization and workforce efficiency, collaborative design and production tools supporting the engineer with data insights.

Cyber security

Cybersecurity risk is a core concern for the manufacturing company, as downtime is incredibly expensive and major damage could be done if rogue actors gain control over equipment and systems. At the same time, lack of sufficient cybersecurity software is a core barrier to further digitization and automation. We’re excited about vertical solutions tending towards industrial players.

Logistics and supply chain

This area within industrial space has received the most VC funding over the last few years, and for a good reason. Industrial logistics still holds on to many analog and manual processes, and we’re excited about solutions creating more transparency in inventory and across the whole supply chain.

Backing the next Nordic industrial champions

The Nordic countries have a multitude of generational industrial companies such as SAAB, Sandvik, Atlas Copco, Vestas, Nokia and Aker across a wide range of industrial and manufacturing areas. Moreover, the industrial complex has since long worked with Nordic top-tier academic institutions providing fertile ground for academic spinouts. This shows in the data, as Speedinvest/Dealroom’s eminent report (source) finds that 32% of all enterprise value created in industrial startups comes from academic roots, as compared to 6% for all startups.

As we’ve learned, founders with a good understanding of the domain have a large advantage building in this space, due to the complex industrial environment. At Inventure, we’re leaning into complexity with our origins in deep-tech investing and having invested in everything from atomic-scale semiconductor surface engineering to energy storage systems, we’re continuing to invest into the re-industrialization of Europe.

If you’re either investing or building in the space, please get in touch!